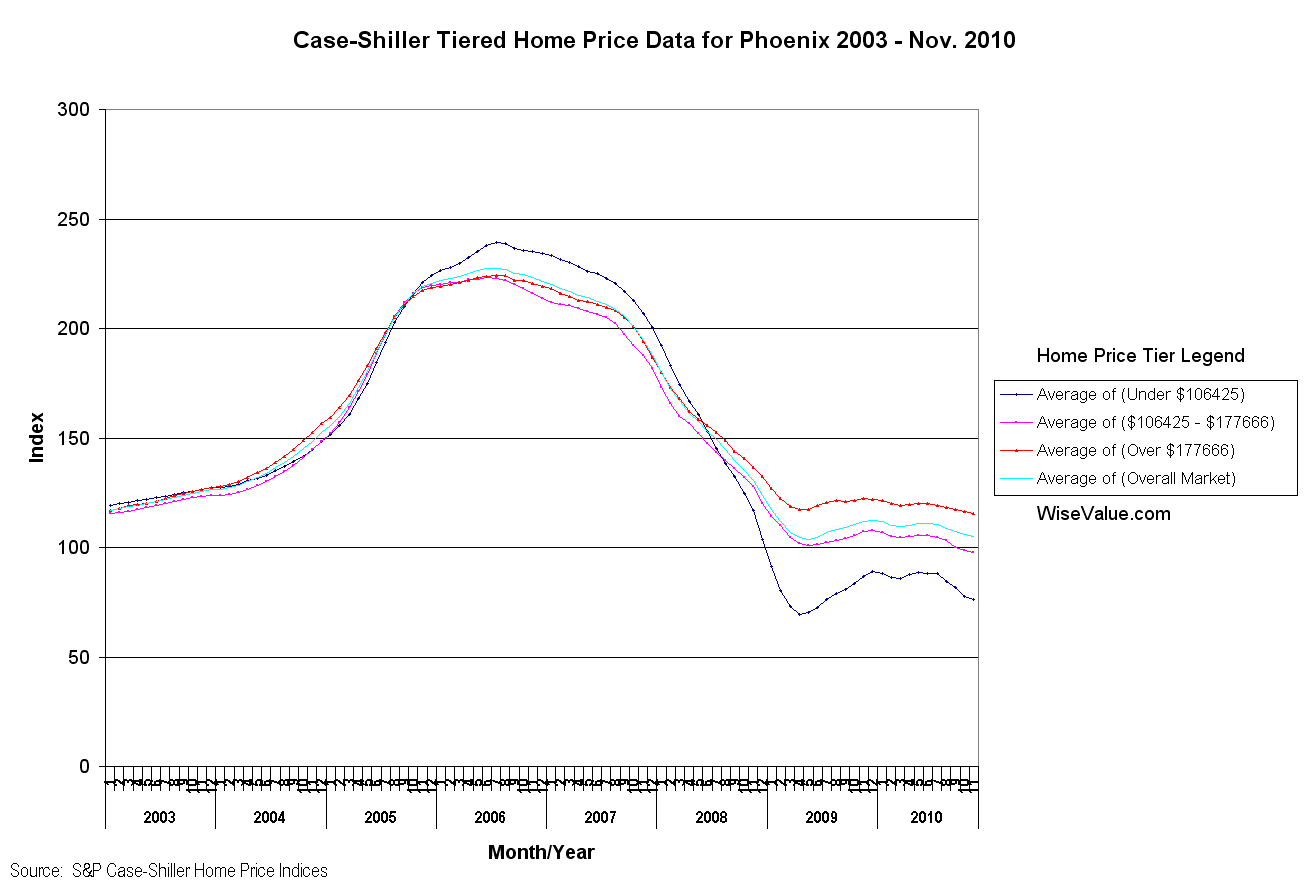

October 2012 housing numbers: Good news for Phoenix Homeowners

November 19, 2012, the National Association of Realtors reported a median price increase of 11.1 percent year-over-year and 5.4 month housing supply for the nation. Twenty nine percent of these transactions were reported to be “all cash” sales, which should add stability to this rising market.

As covered last week in Housing Inventory Drop is ‘Old News’ for Phoenix, inventory in the Valley of the Sun is very low – with only a three month supply valley-wide. These factors, along with an already appreciating market, favorable interest rates and a Fed Chairman pushing for less stringent home loans, set the premise that the Phoenix housing market looks ready to ramp.

Excerpt below from Fed Chairman Ben S. Bernanke on Challenges in Housing and Mortgage Markets

“The Federal Reserve’s Senior Loan Officer Opinion Survey on Bank Lending Practices indicates that lenders began tightening mortgage credit standards in 2007 and have not significantly eased standards since.”

“Certainly, some tightening of credit standards was an appropriate response to the lax lending conditions that prevailed in the years leading up to the peak in house prices….However, it seems likely at this point that the pendulum has swung too far the other way, and that overly tight lending standards may now be preventing creditworthy borrowers from buying homes, thereby slowing the revival in housing and impeding the economic recovery.”

If banks follow through and ease credit, even more money will be chasing an already tight supply of housing.

Big money confirms positive sentiment, with the purchase of 563 acres in Mesa cited as one recent example. While there are contingent factors like interest rates, how the approaching Fiscal Cliff and solvency issues of FHA are handled, the Phoenix housing market looks bright from here.

Comments Off